San Francisco Restaurant

“It’s great that workers can take their plan with them when they leave, with no rollover or anything. And it’s one less thing for me to worry about.”

Step into the future of retirement

The PRP is easy to use, affordable, and completely removes the plan sponsorship burden.

Icon’s PRP gives you and your employees what the 401(k) never could — simplicity, freedom, and true portability.

Employers are switching from 401(k)s to the PRP because it’s faster to launch, easier to run, and costs about half as much.

Discover why the PRP is one of the fastest growing plans in the country.

The Benefit Without the Burden

San Francisco Restaurant

“It’s great that workers can take their plan with them when they leave, with no rollover or anything. And it’s one less thing for me to worry about.”

$1,800

Saved annually

40 min

To implement

20 min

Of admin time monthly

Los Angeles Health Care Services

“It works like a 401k plan but for 1099 contractors, this is a huge help to our business.”

350

Full time 1099 employees

$8,640

Dollars saved annually

2

Hours to implement

“The transition from our 401(k) really has been easy, and now we can offer our employees best of class benefits without the high costs and headaches. This is a big win for our agency and caregivers.”

New York City Hospitality Group

“We didn’t know a plan like this existed!”

300

Full time W-2 employees

$7,440

Dollars saved annually

4

Hours to implement

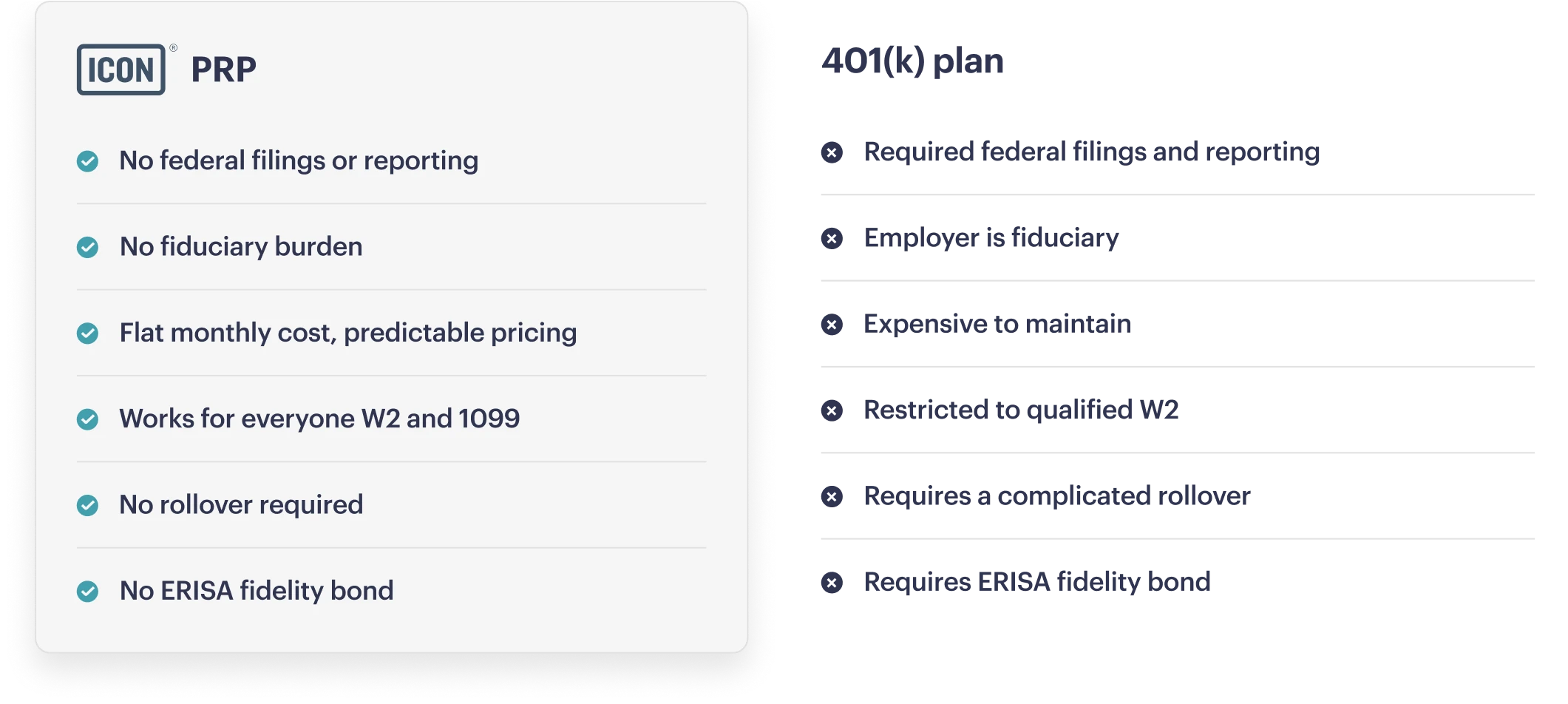

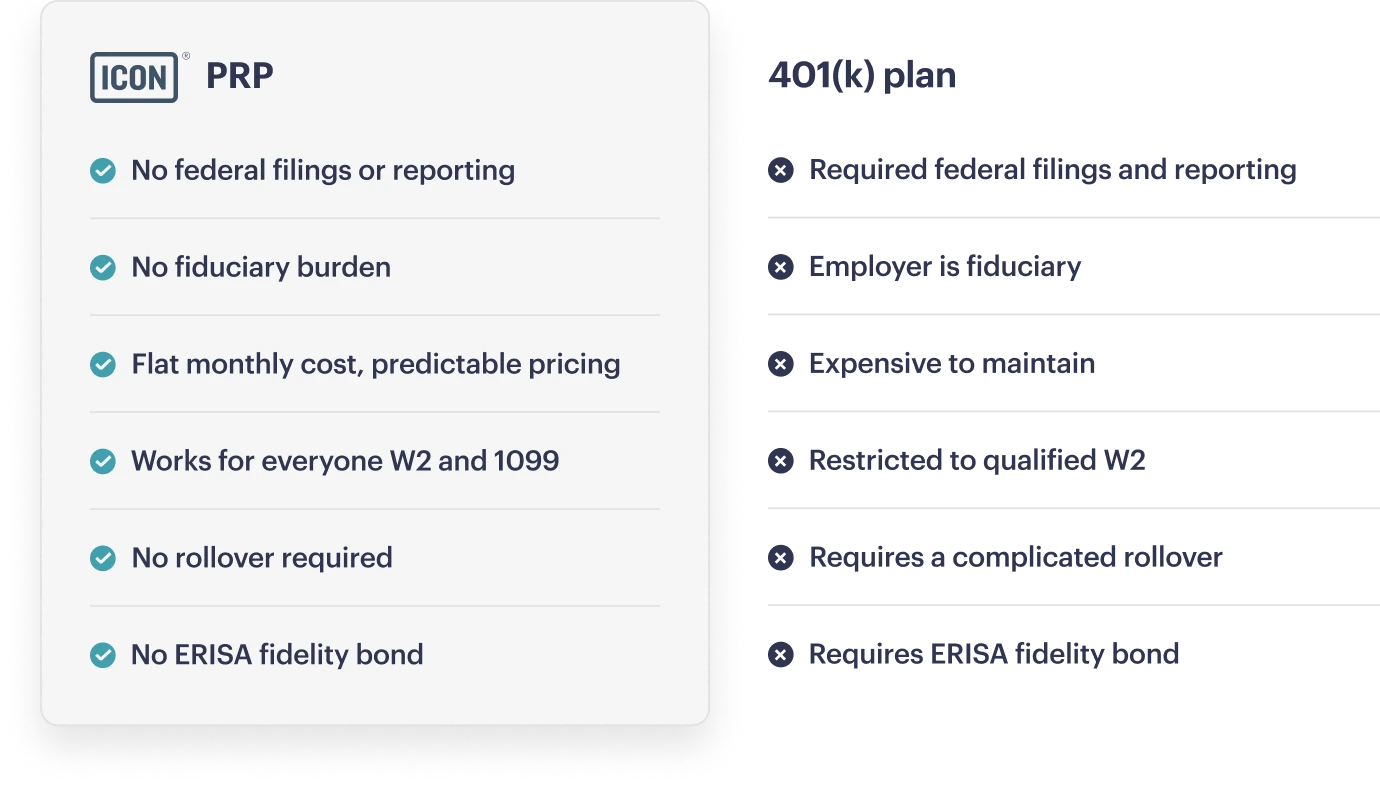

The Portable Retirement Plan (PRP) is a modern retirement benefit that’s easy and affordable for employers to offer and simple for employees to use. The PRP works like a 401(k), with tax-advantaged savings and automatic payroll contributions — but without the administrative burden. No plan sponsorship. No federal filings. No ongoing maintenance.

Icon is a retirement benefits platform for small and mid-sized employers. We help companies offer a portable, payroll-friendly plan people actually use—high-quality experience for employees, streamlined administration for employers, and no surprise fees.

Both plan types have tax-advantaged savings and automatic payroll contributions. But the PRP removes the headaches that come with 401(k) plans. A 401(k) is an employer-sponsored plan, which makes the employer the plan sponsor and a fiduciary. A 401(k) limits participation to W-2 employees under the plan’s rules, and triggers ongoing obligations like nondiscrimination testing, Form 5500 filings, and other ERISA reporting and disclosures. When employees change jobs, they typically need to roll over or cash out their 401(k) to consolidate—adding friction and risk. By contrast, with the PRP, the employer simply enables payroll contributions without becoming a plan sponsor or taking on fiduciary oversight and complex annual filings. The employee’s PRP is in their name, so their account stays with them when they change. The result is a high-quality, payroll-integrated benefit that covers more of your workforce (including part-time) with far less administrative lift—and it can also run alongside an existing 401(k) if you want both options.

It's easy. We'll help you set up your PRP - it only takes about 30 minutes. You can work with your 401(k) provider to terminate your 401(k). Your PRP can be launched before, during, or after you terminate your 401(k). Some clients choose to offer both the PRP and a 401(k) as an additional way for employees to save.

Yes. Icon is built to work seamlessly with any payroll provider, ensuring effortless connectivity across all systems. For select platforms, we’ve developed custom integrations that optimize data flow, enhance automation, and streamline your payroll and admin work.

We're happy to set up a quick call to answer your questions.