Developing a plan to save for retirement can feel daunting. The idea is basic enough: set aside money each month or year, invest it, then use it once you retire. But how much you should set aside and where you should invest it and through which vehicle (e.g. IRA, 401k, etc.), to ensure you’ll have enough money in your golden years is complicated. And the answers change constantly depending on your financial and employment situations.

That’s why 401k calculators are functionally useless.

What is a 401k Calculator?

A 401k calculator is a tool that many financial institutions provide to show you how much you should be saving each month in order to reach a certain retirement goal. It usually takes into account basic inputs like:

- Your age,

- Your 401k balance (if any),

- Annual income,

- Percent contribution,

- Employer matching,

- Retirement age,

- Average rate of return,

- Investment fees as a percent. Note: they typically leave out administrative fees which can be substantial.

Then the calculator will spit out a combination of the following predictions:

- Your monthly costs in retirement,

- Your 401k balance when you retire,

- How much of your monthly costs your 401k will cover, and sometimes

- How much you’ll pay in fees over the course of your working life.

What a 401k Calculator Actually Shows You

You might look at the above list, and think, “That’s useful information.” And it is in the sense that it’ll give you a basic idea of what happens to your savings as you continue to contribute and invest it in the market, and just how far fees can erode your savings. But here’s the hard truth: a 401k calculator is only a snapshot of what your retirement savings journey looks like right now using a standardized set of assumptions.

For instance, you might live in a high cost of living state during retirement, in that case you might need more per month in living expenses than the calculator predicts. Conversely, you might own your home outright and have very low monthly expenses at retirement. It also doesn’t take into account any other investments you might make over the course of your working life or health issues you could develop that need managing. So the calculator’s predictions can only give you a vague, general idea of what your financial situation in retirement could, potentially, maybe look like if everything stayed exactly the same as it is right now.

We don’t have to tell you that this is an unrealistic expectation because, to quote the Greek philosopher, Heraclitus, “Change is the only constant in life.” As you earn raises, suffer unemployment, experience highs and lows in the market, change employers and your contribution percentage, change investment portfolios or perhaps roll your savings into a different savings vehicle, that original snapshot becomes outdated and therefore, irrelevant.

What’s Better than a 401k Calculator? Understanding How Compounding Affects Your Balance

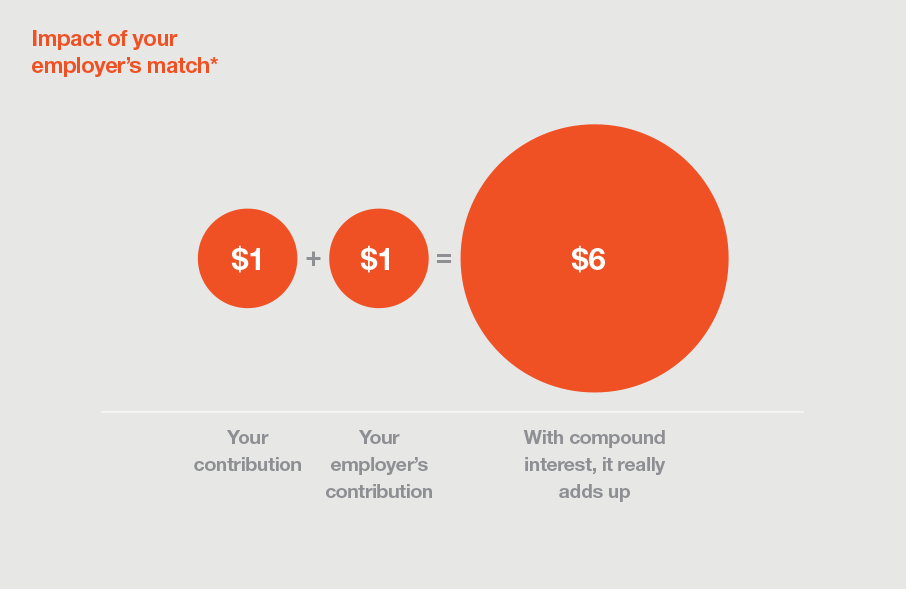

The important thing to understand about saving for retirement is: the more you save (and the earlier you start), the more you earn in the market because of something called “compounding”. Compounding is what happens when the interest you earn on your principal contributions earns interest.The more frequently your money compounds, the faster it grows without any additional contributions.

It’s all about compound interest. Use the slider to see how what you set aside today can grow over time.

$7

Adds up over time with compound interest*

Another Important Thing to Understand: High Fees Erode Savings Quickly

Employer sponsored retirement savings plans are often subject to two types of fees: investment fees and administrative fees. Investment fees are what the financial institution charges for managing your portfolio of investments. The average investment fee ranges from 0.58% to 1.2% of the portfolio balance, depending on the type of fund you’re invested in.

In addition to investment fees, employers typically pass on the cost of managing the plan (i.e. administrative fees) to account holders. The administrative fees charged to individual account holders will depend on the employer, the financial institution investing the retirement plan, the company that’s actually managing the plan (this could be the employer, the financial institution or a third party), and the portfolio the savings account is invested in.

How Do I Make Sure I’m Saving Enough?

There are a few different philosophies out there and each espouses a different ideal budget percent allocation. What some people do is, take your total monthly take-home pay for your household (for 1099 employees, this is your gross pay net of taxes, for W-2 employees, this is your paycheck), and allocate the money accordingly:

- 70% for expenditures (needs + wants)

- 20% for saving (retirement savings and saving for big purchases like a house)

- 10% for your emergency fund (for unexpected crises like unemployment or a medical emergency), debt repayment or donations

This isn’t a hard and fast rule and your actual percentages will likely fluctuate depending on your current circumstances. But aiming to save some of your income is a good way to build financial health and ensure that you’ll not only be taken care of in retirement, but in a crisis as well.