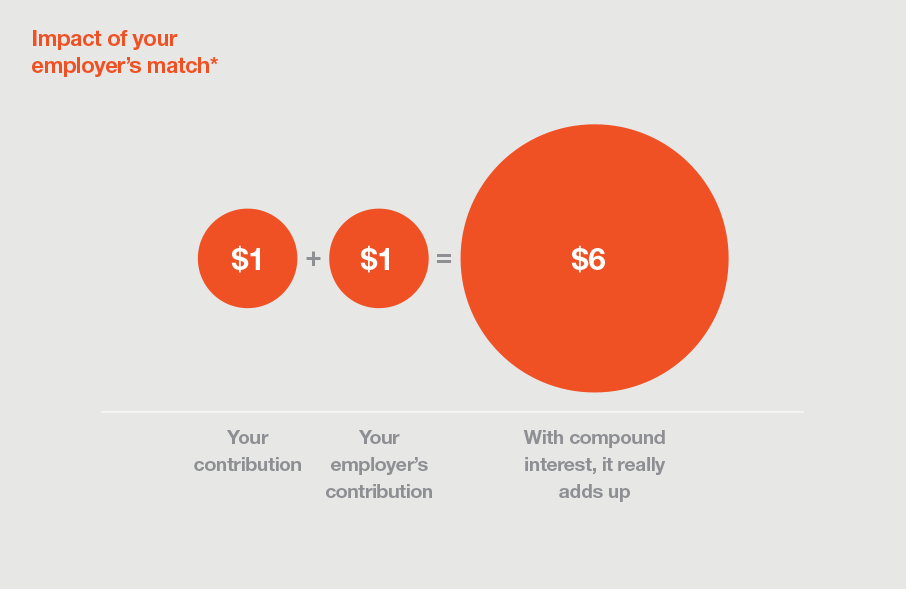

It’s not very often in life that someone will pay you to save money, but a 401(k) match is one of them. A 401(k) match is when an employer contributes, dollar-for-dollar, the same amount you put into your 401(k). Many employers offer this benefit up to a certain limit (e.g. 6% of your annual compensation).

That means the more money you contribute each pay period (up to the limit), the more of a match you get. And the more of a match you get, the more money you have to invest and the faster your investments grow because of compound interest. So if your employer offers any type of matching, you should try to contribute up to the matching limit so you don’t leave any money on the table.

Alternatively, your employer is not required to match your 401(k) contributions or it might require you to work for the company for a minimum period of time before you get to keep all of the contributions they’ve made on your behalf. The process of releasing the contributions made on your behalf is called vesting. Many companies will have incremental vesting thresholds, so the longer you work for them, the greater the percentage of their contributions you “own”.

Matching formulas and policies vary from company to company so if you have any questions about your company’s plan, reach out to your manager or HR department.

* This illustration is a hypothetical compounding example that assumes biweekly deferrals (for 30 years) at a 7% annual effective rate of return. It illustrates the principle of time and compounding. It is not intended to predict or project the investment results of any specific investment. Investment returns are not guaranteed and will vary depending on investments and market experience. If fees, taxes, and expenses were reflected, the hypothetical returns would be less.

Many companies are now offering auto-escalation in their 401(k) plans. With auto-escalation, your contribution level is automatically increased at regular intervals, typically 1% a year, until it reaches a preset maximum.

Another version of this is a program called SMarT, which stands for Save More Tomorrow. Under the SMarT program, employees agree today to increase their 401(k) contribution rate in the future, generally when they receive their next raise. SMarT is an easy, painless way to set yourself up for regular contribution increases that coincide with pay increases, so you don’t feel the pinch of saving more.

If either of these automatic savings options sounds attractive to you, ask your employer whether your plan has an auto-escalation or SMarT feature.

We often associate high cost with high value, and while this can work for cars, phones, and other goods and services, it is not true for the fees you pay to manage your investments. In fact, high fees have a corrosive impact on your savings.

Over time, high fees will eat away at the value of your account, leaving you with less money in your retirement years. To understand how fees affect you, the individual investor, consider the following example:

Types of fees

If you are in an employer-sponsored plan such as a 401(k), 403(b), or 457 plan, you can expect to pay the following fees.

Investment fees. These are the fees charged by mutual fund companies to pay for the costs of managing 401(k) plan investments. These are the largest fees you pay and are charged annually as a percentage of your account balance.

A typical percentage is 0.63%, but it isn’t uncommon to find fees ranging from the low end of 0.25% to well over 1.3%.

Plan administration fees.These are the expenses involved in the day-to-day operation of running a 401(k) plan, including recordkeeping, accounting, online access, and customer service. The administration fees may be charged by the financial company that manages your plan investments (the “plan provider”) or by an outside company hired by your employer to handle the administration of the plan.

To ensure you have the most money available to you in retirement, you want to look for an investment vehicle with low annual fees. If your employer doesn’t offer a 401(k) fund with low fees, consider rolling your savings into a low-cost IRA like Icon.

* All figures in 2012 dollars. Workers are assumed to begin saving at age 25 and retire at age 67. Example reflects median salary of $30,502 when worker starts saving at age 25. Example provided by CAP.

Retirement accounts allow you to name “beneficiaries,” or people or organizations that will receive your retirement savings in the event of your passing.

Selecting beneficiaries is an important step in securing the future of your savings. If no beneficiaries are indicated and you pass away, your retirement account must go through the complicated probate process instead of going directly to your loved ones or preferred organizations.

How to designate a beneficiary. Most financial institutions make the process of selecting beneficiaries easy by providing you with a straightforward form that allows you to indicate one or more desired beneficiaries, and the percentage of money they should receive in the event of your passing. There is typically no limit to the number of beneficiaries you can indicate, so you can allot different amounts to several recipients of your choice. People generally choose their spouse or children; however, siblings, close friends, other individuals, or organizations can be selected as well.

Beneficiary forms usually require some basic information about the intended beneficiaries, as well as their Social Security or tax ID. The requirements to designate a beneficiary or beneficiaries vary by company so it’s a good idea to ask the servicer of your retirement savings about its specific policy.

Generally speaking, it makes sense to consolidate old 401(k) and 403(b) plans into one place. But there are a couple instances when it might make sense to leave your money where it is. Let’s look at both cases.

Advantages to consolidation:

Simplicity. Having all of your money in one place makes it easier to manage your investments, as you have to pay attention to only one account.

Fees. One account is almost always less expensive than multiple accounts.

Investment freedom. If your money is with an old employer’s plan, you are limited to the investments available in that plan. If you invest in an IRA, you have more choices.

Safekeeping. It’s not uncommon for people to lose track of their old plans.

Why you might want to keep your separate accounts:

Low fees. If your previous employer has a great plan with low fees, it might make sense to leave your savings in their plan, especially if you are nearing retirement.

Tax reasons. In rare cases, there could be good tax reasons to leave your money behind.

To decide if consolidating your retirement accounts is right for you, look at your personal circumstances and consult a tax advisor if necessary.