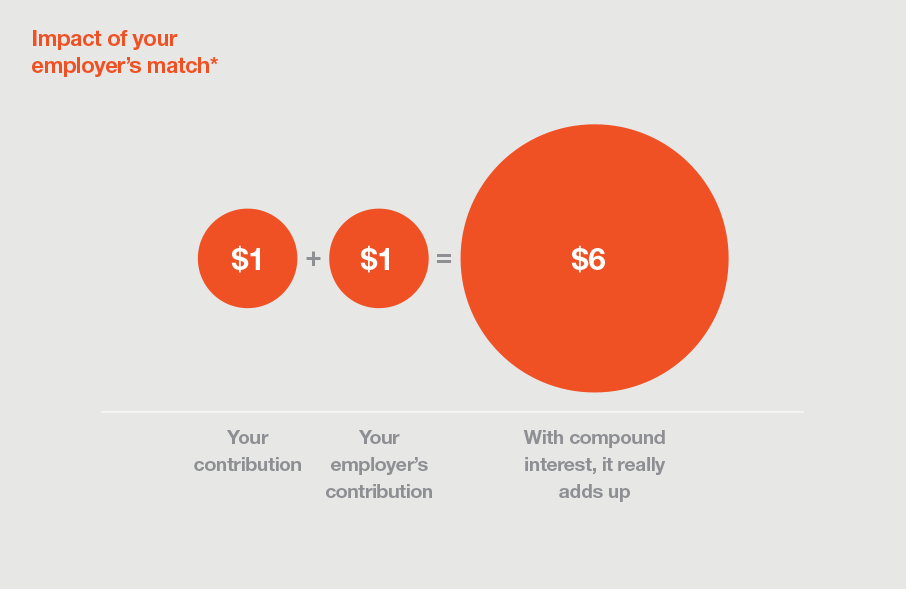

It’s not very often in life that someone will pay you to save money, but a 401(k) match is one of them. A 401(k) match is when an employer contributes, dollar-for-dollar, the same amount you put into your 401(k). Many employers offer this benefit up to a certain limit (e.g. 6% of your annual compensation).

That means the more money you contribute each pay period (up to the limit), the more of a match you get. And the more of a match you get, the more money you have to invest and the faster your investments grow because of compound interest. So if your employer offers any type of matching, you should try to contribute up to the matching limit so you don’t leave any money on the table.

Alternatively, your employer is not required to match your 401(k) contributions or it might require you to work for the company for a minimum period of time before you get to keep all of the contributions they’ve made on your behalf. The process of releasing the contributions made on your behalf is called vesting. Many companies will have incremental vesting thresholds, so the longer you work for them, the greater the percentage of their contributions you “own”.

Matching formulas and policies vary from company to company so if you have any questions about your company’s plan, reach out to your manager or HR department.