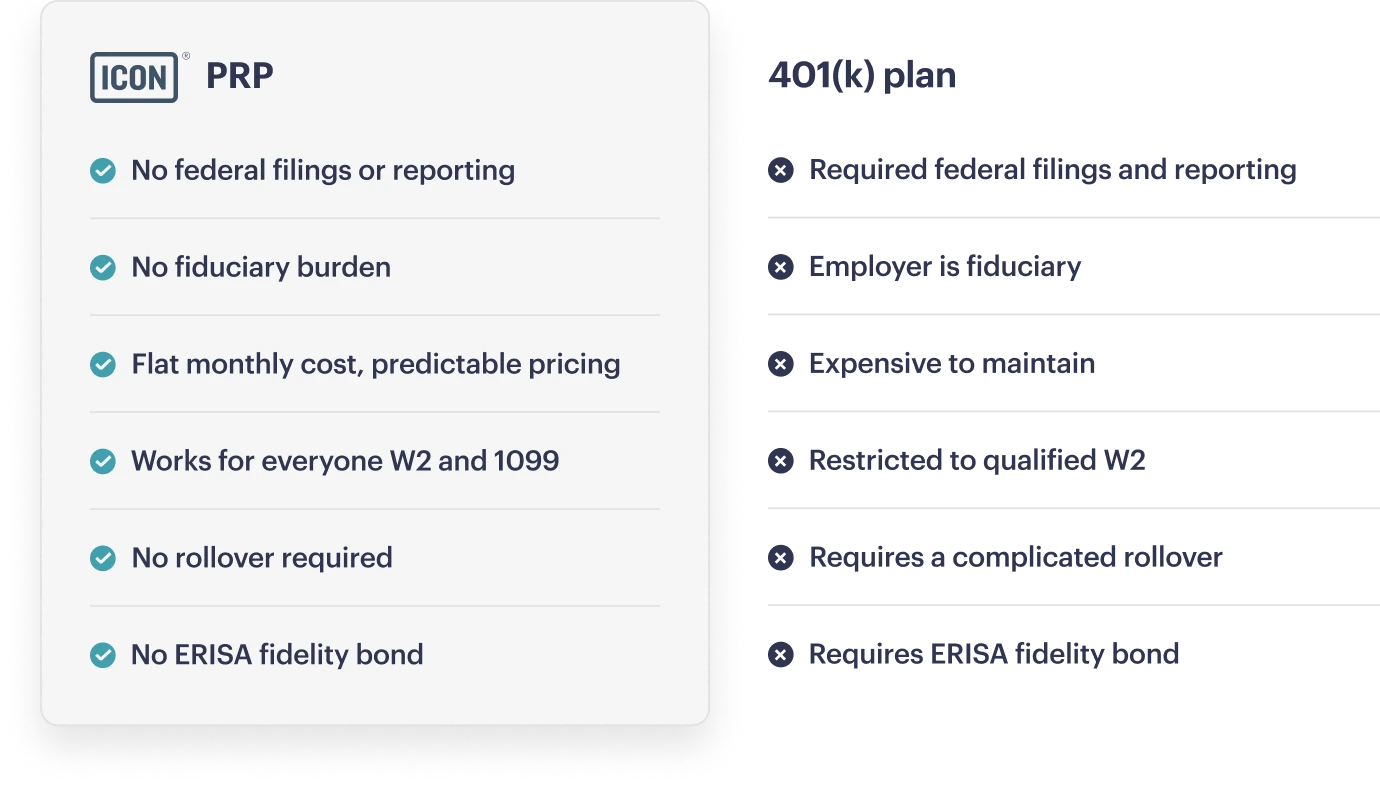

Not Like Traditional Plans.

Straightforward pricing.

Icon offers flat monthly pricing, based on the number of employees at your company, enrollment is unlimited.

The PRP by Icon.

PRPs offer a plan packed with features but without the high-cost, hidden fees, and ancillary costs that come with traditional plans.

Icon offers flat monthly pricing, based on the number of employees at your company, enrollment is unlimited.

Our platform handles all of the record keeping and transactions.

We handle inviting employees to create their account and enroll in the plan.

Icon takes care of employee communications and provides financial education information.

Icon is a fiduciary. We recommend a portfolio tailored to the employee and handle all portfolio management.

We provide regular account statements as well as the documents needed at tax time.

Employers can easily get an overview of their plan, including total contributions to date and participation metrics.

San Francisco Restaurant

”It’s great that workers can take their plan with them when they leave, with no rollover or anything. And it’s one less thing for me to worry about.”

$1,800

Saved annually

40 min

To implement

20 min

Of admin time monthly

The Benefit Without the Burden

Take the first step toward offering an affordable, hassle-free retirement solution for your business.