Having a retirement plan is one of the most effective ways to reduce financial stress and feelings of fragility for workers. But there’s a structural problem: Most small and mid-sized businesses can’t offer a 401(k) because it’s too expensive, too complex, and too burdensome to administer.

Morningstar’s long-term analysis makes the issue impossible to ignore: Nearly 80% of small 401(k) plans shut down over a 10-year period due to cost and complexity.

The system is simply not built for SMBs — and workers pay the price.

At the same time, financial pressure on employees is rising fast. New research from The Harris Poll shows that even high earners are feeling strained — with one in three six-figure earners saying they’re stretched or drowning financially, and many feeling “one unexpected bill away from chaos.” In this environment, retirement benefits matter more than ever. But the legacy 401(k) system is failing both employers and employees.

The 401(k) Has a Design Problem — And Employees Are Paying for It

The Wall Street Journal recently highlighted a major flaw: workers lose investment growth simply because they switch jobs.

Here’s what happens today:

When an employee leaves with a small 401(k) balance, employers can force-roll the money into a low-yield IRA.

These “safe harbor IRAs” often earn less in interest than they charge in fees.

EBRI estimates they hold $28B today, growing to $43B by 2030 — money sitting idle instead of compounding.

This isn’t employee mismanagement. This is a design flaw in the employer-sponsored system — a system built for 1978, not 2025.

Employees Need Stability. Employers Need Simplicity. The 401(k) Offers Neither.

Today’s workforce is:

financially stressed

mobile

digitally fluent

and seeking benefits that actually support their financial lives

But the 401(k) creates friction at every job change, piles administrative work on employers, and is simply too costly for many SMBs to sustain.

That’s why so many plans shut down. And it’s why employers are looking for a better alternative.

The PRP by Icon: A Simpler, Modern Retirement Benefit

The PRP is built for the realities of today’s workforce and today’s employers.

1. Half the cost of a 401(k)

No plan sponsor liability. No plan testing. No administrative burden.

2. Lower participant fees

Workers keep more of what they save — critical in a time when even six-figure earners feel squeezed.

3. A plan that follows the person, not the employer

Employees keep the same account and investments across jobs. No forced rollovers. No stranded savings. No lost compounding.

4. Seamless and easy to use

Modern, digital, fast — designed for workers who manage their lives on their phones, not through paperwork packets.

The takeaway for employers

Offering a retirement plan shouldn’t require legal exposure, high costs, or a full-time administrator. And your employees shouldn’t lose money simply because they changed jobs.

The PRP by Icon gives employers a low-cost, low-burden way to offer a benefit that actually strengthens financial stability — without inheriting the problems baked into the old system.

Affordable. Portable. Modern. A retirement benefit finally built for the world we live in today.

Contact an Icon Retirement Specialist today to learn more.

Innovative partnership delivers modern retirement benefits to thousands of QSR workers across iconic brands

San Francisco, California—August 7, 2025 — GoTo Foods, the centralized supply chain and innovation arm powering iconic restaurant brands like Jamba Juice, Cinnabon, Carvel, and Auntie Anne’s, has partnered with Icon to bring modern, portable workplace retirement benefits to franchisees and their employees across the U.S.

This partnership makes Icon the preferred retirement solution for GoTo Foods franchises, providing immediate compliance with state mandates and delivering a retirement plan designed specifically for high-turnover industries like quick-service restaurants (QSR).

“Franchise owners are navigating a competitive job market, growing compliance requirements, and shifting employee expectations,” said Laurie Rowley, CEO of Icon. “The PRP gives GoTo Foods’ franchisees a modern, easy, and affordable way to offer a top-requested benefit without taking on the high-cost, complexity, or risk associated with 401(k) plans.”

A Retirement Plan Built for Restaurants

The 401(k) plan was created fifty years ago as a supplement to a pension for large corporations; they are not a one-size fits all plan. The PRP isn’t a better 401(k); it’s a complete redesign of retirement purpose-built for today’s workforce including hourly and part-time employees—many of whom are saving for retirement for the first time. With zero administrative burden, no required plan audits or filings, and personalized investing, franchisees can offer a top requested benefit that builds employee loyalty without draining resources.

Key benefits for GoTo Foods franchisees include:

Flat monthly pricing— low cost transparent pricing with no hidden fees

Fully-managed plan— turnkey plans require no paperwork or fiduciary responsibility

Portability—savings stay with employees across jobs with no rollovers required

Attraction & retention—offer a benefit hourly employees actually use

Compliance with state retirement mandates

GoTo Foods’ supply chain supports over 9,400 restaurant locations globally, and nearly half of U.S. franchises now fall under state retirement mandates. Icon’s solution ensures operators stay compliant while supporting their teams with a benefit that meets the moment.

Choosing the best 401k for your small business can be overwhelming. Between fiduciary risks, compliance, and hidden fees, many small business owners are now exploring simpler, low-cost retirement alternatives.

What Makes 401k Plans Expensive for Small Businesses?

Even the best 401k plans can create challenges for businesses:

You become the plan sponsor. You’re responsible for compliance, filings, and fiduciary liability. Most businesses don’t realize they hold the fiduciary responsibility and legal risks.

Costs stack up. Monthly fees, per-employee charges, and required employer match add up fast.

Setup is complex. Paperwork, plan design, and IRS filings slow things down.

Ongoing compliance is heavy. Annual testing, government filings, and possible audits create risk.

Employees face rollovers. When they leave, accounts may be cashed out, lost, or forgotten.

Key Questions Before Choosing a 401k for Your Small Business

Who handles compliance and testing?

What happens if your workforce grows or shrinks?

Can you afford a required match for every eligible employee?

What is the true long-term cost in money and time?

The Alternative: Icon’s Portable Retirement Plan (PRP)

Instead of sponsoring a 401k, many small businesses now choose the PRP — a fully managed, low-cost retirement plan designed for today’s workforce.

No fiduciary responsibility. No plan sponsorship burden risk.

No filings or audits. No ERISA requirements or government paperwork.

Affordable and simple. One flat monthly fee, no required match.

Works for all types of workers. W-2, 1099, part-time, and full-time.

Fully portable. Employees keep their account even when they leave.

Compare: PRP vs 401k

Feature

Icon PRP

401k Plan

Employer role

No sponsorship or fiduciary duty

You’re the sponsor and fiduciary

Setup

Fully digital, ~30 minutes

Paperwork-heavy, slow

Compliance

No filings or audits

Annual filings and testing

Cost

Flat monthly fee

Monthly, per-employee, plus match

Eligible workers

W-2, 1099, part-time, full-time

W-2 only

Portability

Employees keep their account

Rollovers required when they leave

Why Small Businesses Choose the PRP

✅ No legal or fiduciary burden ✅ No filings or ERISA compliance ✅ Low-cost, no required match ✅ Flexible for any workforce ✅ Employees keep their retirement savings

The Best 401k for Small Business? Here’s the Bottom Line.

If you’re looking for the best retirement plan for your employees, consider this:

What if the right plan for your business isn’t a 401k at all?

The PRP may offer a simpler, more affordable way to help employees save — without the headaches of a 401k.

Businesses should consider their needs and look for a plan that suits them. Be sure to consider 401k alternatives and look at the plan cost, complexity, and compliance requirements.

What makes the PRP easy to use?

The PRP takes the headaches out of offering a retirement benefit. There’s no required match, no annual testing or audits, and no compliance maze to navigate. It’s simple to set up, easy to manage, and designed to work for your business—not against it.

Is the PRP portable?

Yes. With the PRP, employees keep their retirement savings when they leave—no paperwork, no abandoned accounts. It’s their plan, not the company’s. That means you’re giving them something that actually supports their future.

California law currently requires all employers with 5 or more employees to offer a retirement plan.

The deadline to comply was June 2022.

Starting in 2025, employers with 1 or more employees will have to offer a retirement plan.

The state can impose fines of up to $750 per employee for failure to comply.

To comply, employers can offer a retirement plan through a provider of their choice, or use the state-run plan.

This guide will help you understand what CalSavers is and who it applies to, along with what you need to do to comply.

What is a The Retirement Mandate law in California?

California law makes it mandatory for employers with 5 or more employees to provide a retirement savings plan to their employees. The deadline was June 2022, and employers not complying are subject to fines. Starting in 2025, this law will apply to any employer with at least one employee in California. The law is meant to help combat the retirement savings crisis prevalent in the state, where nearly half of private sector employees lack access to retirement plans at their workplace.

What is CalSavers?

CalSavers is the name of the state-run retirement plan. It was designed to provide a retirement savings option for employers that don’t offer a retirement plan and don’t want to offer a plan through a retirement plan provider. The program is funded by employee contributions, which are deducted automatically from their paychecks. CalSavers is a payroll deduction Roth IRA, which means contributions are made post-tax.

How Does CalSavers Work?

As an employer using CalSavers, you’ll have some steps to take to get started along with ongoing responsibilities. After you register for CalSavers, you’ll need to upload your roster of eligible employees. Then, your role in the CalSavers program is to facilitate your employees’ contributions. This means you’ll need to deduct the contributions from your employees’ paychecks and send them to CalSavers. You’ll also need to manage your employees’ enrollment in the program, including tracking who’s participating and who’s opted out.

Remember, you’ll have the ongoing responsibility of keeping your account current. This means you need to update employee contribution rates when employees make changes, add new employees within 30 days of their hiring or when they become eligible, and mark employees as inactive if they leave or are terminated. Additionally, you’ll continue to process payroll contributions for participating employees.

Who Needs to Comply with CalSavers?

If you’re an employer with 5 or more employees in California and you don’t already offer a retirement plan, you’ll need to register with CalSavers or offer a retirement plan through a provider of your choice. If you don’t, you could face steep penalties. The penalties for non-compliance start at $250 per employee and can go up to $750 per employee.

CalSavers compared to 401k plans and PRPs

CalSavers is not your only choice when it comes to offering a compliant retirement benefit. The two other plan types that comply with the mandate are a 401k and a PRP.

The familiar 401k plan was created to replace pension plans at large companies. It allows employees to contribute a portion of their income, pre-tax, into a retirement account. Many small businesses find that the 401k is cost-prohibitive and that they don’t have the resources to manage them. As an employer sponsoring a 401k plan, you become a fiduciary to your employees and can be sued if you don’t act in the best interest of the plan participants.

PRPs (Portable Retirement Plans) are a new type of retirement plan offered by Icon. PRPs work like a 401k but without the high cost, regulatory complexity, and fiduciary burden. Both 401k plans and PRPs offer tax-advantaged savings and automatic payroll contributions, but PRPs have some big advantages:

No federal filings or reporting

No fiduciary burden

Flat monthly cost, predictable pricing

No rollover required

No ERISA bond

The PRP by Icon is an easy and affordable way to meet the California mandate. With a PRP you can meet the California retirement mandate and provide your employees with a valuable retirement savings plan without the hassle and complexity of 401k plans.

Frequently Asked Questions

1. How can I ensure I’m in compliance with the California retirement mandate?

To ensure you’re in compliance with the mandate, you can either offer a qualifying retirement plan (like the PRP by Icon) or register to facilitate CalSavers. If you choose to offer a PRP, we’ll provide the documentation you need to show you’re in compliance.

2. How does the PRP compare to CalSavers?

PRPs by Icon are fully automated, removing the administrative burden from employers. You can set up your plan in minutes, and we integrate with your banking and payroll partners. Once you launch your plan, we handle the rest, including employee enrollment and communications. You’ll get access to your employer dashboard so that you can easily review and monitor your plan.

CalSavers offers a limited number of investment options. With Icon, employees get a portfolio tailored to their needs, giving them a more personalized plan that is managed for them. Plus, while CalSavers may not cost employers any money, the fees charged to employees are higher and the employer will spend their time with the ongoing responsibilities of managing CalSavers.

3. How can I get started with Icon?

Getting started with Icon is easy. Just visit our website, click on “Get Started,” and follow the prompts to set up your plan. We’ll guide you through the process and provide all the support you need. Signing up only takes about 5 minutes.

4. What if I already offer a retirement plan to my employees?

If you already offer a retirement plan, you can still switch to Icon – it’s easy, and we’ll help you make the change

5. What are the benefits of offering a retirement plan to my employees?

Offering a retirement plan can help attract and retain top talent, improve employee satisfaction, and provide a tax-advantaged way for your employees to save for retirement.

6. How can I educate my employees about retirement savings?

If you choose Icon’s PRPs, we provide educational resources and support to help your employees understand their retirement savings options. Educating your employees about retirement savings is important for their financial future.

7. What if my business grows and I have more employees?

With Icon, we scale with you. Whether you have 5 employees or 500, we make it easy to offer a retirement plan.

Get in Touch

We’re here to help! If you have any questions or need a hand navigating your retirement plan options, don’t hesitate to get in touch with us. We’re here to help you find the best solution for your business.

As a small business owner, you want to take care of your employees, grow your company, and stay ahead of the competition. But let’s face it: the 401k, especially for small businesses, is outdated. It’s expensive, complicated, and designed for a corporate world that no longer exists. It’s time to rethink retirement benefits, and that’s why the Portable Retirement Plan (PRP) was created. It’s the solution built for the future.

Why the 401k Fails Small Businesses

Here’s the truth: 401k plans were not designed for small businesses. They were created for massive corporations that have the resources to manage the legal hoops, compliance testing, and fiduciary risks. Most small business owners simply don’t have the time, money, or bandwidth to deal with the complexities that come with offering a 401k.

Here’s why small businesses struggle with 401ks:

High Costs: From administrative fees to compliance and investment management costs, a 401k plan is expensive to maintain. For small businesses, these fees can eat up precious resources.

Complex Regulations: 401k plans require adherence to strict IRS and Department of Labor regulations. This includes annual compliance testing to ensure fairness across all employees. Navigating these regulations is time-consuming and a headache for small business owners.

Fiduciary Responsibility: Offering a 401k means you are legally responsible for your employees’ retirement funds. Even if you work with a provider, some fiduciary duties remain on your shoulders, exposing you to potential legal risks.

Limited Flexibility: Small businesses tend to have a mobile workforce with high turnover. Traditional 401k plans don’t offer the flexibility needed for employees who frequently switch jobs, and the rollover process can be a hassle.

Safe Harbor 401k Plans: A False Safety Net

Many small businesses turn to Safe Harbor 401k plans because they automatically pass IRS non-discrimination testing, ensuring the plan benefits all employees, not just the top earners. In fact, 70% of SMBs choose Safe Harbor plans to avoid failing compliance tests.

But here’s the catch: Safe Harbor plans require mandatory matching contributions for all employees, regardless of whether your business can afford it. These contributions typically range from 3-4% of each employee’s salary. So, while Safe Harbor plans save you from compliance headaches, they can significantly increase costs, especially as your business grows.

For a small business, that mandatory match can put a serious strain on resources. The more employees you have contributing, the higher the cost burden on your business.

The PRP: The Game-Changer for Small Businesses

This is where the Portable Retirement Plan (PRP) comes in. It’s a modern, flexible, and affordable alternative to the traditional 401k. Here’s why it works for small businesses:

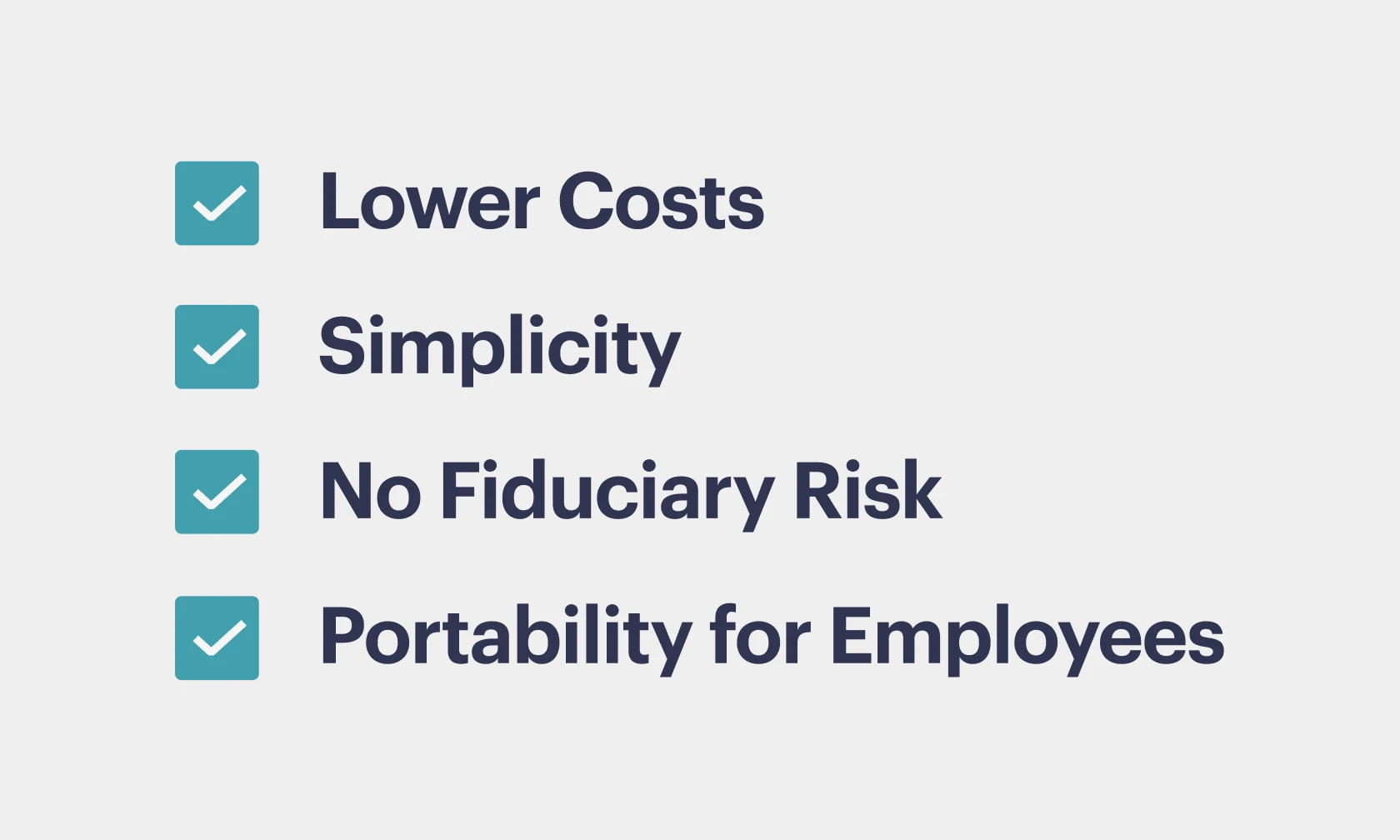

Lower Costs: Forget the surprise fees that come with a 401k. PRPs offer predictable, lower costs with simple, flat fees—whether monthly or annually. You’ll never be blindsided by hidden charges or required matching contributions.

Simplicity: PRPs remove the administrative burden that comes with 401ks. There’s no need for annual compliance testing, and no complicated IRS regulations to navigate. It’s built for ease of management.

No Fiduciary Risk: One of the best things about a PRP is that it eliminates fiduciary responsibility for the employer. When you work with a provider like Icon, they assume fiduciary duties on behalf of your employees, saving you from legal risks and the need for costly fiduciary insurance.

Portability for Employees: PRPs address one of the biggest flaws in the 401k—the portability problem. Employees can take their retirement savings with them wherever they go, without needing to roll over accounts.

Why PRPs are the Future

The PRP isn’t just an incremental improvement. It’s a breakthrough. This is what the 401k should have been—a flexible, affordable, and portable retirement solution for the modern workforce. And now, it’s available to every small business, not just the big guys.

By embracing the PRP, you’re not just offering your employees a retirement plan—you’re providing them with a future. And you’re doing it without sacrificing your time, money, or peace of mind.

So, ask yourself: Do you want to keep using the same outdated tools that hold your business back, or do you want to be part of the future of retirement planning?

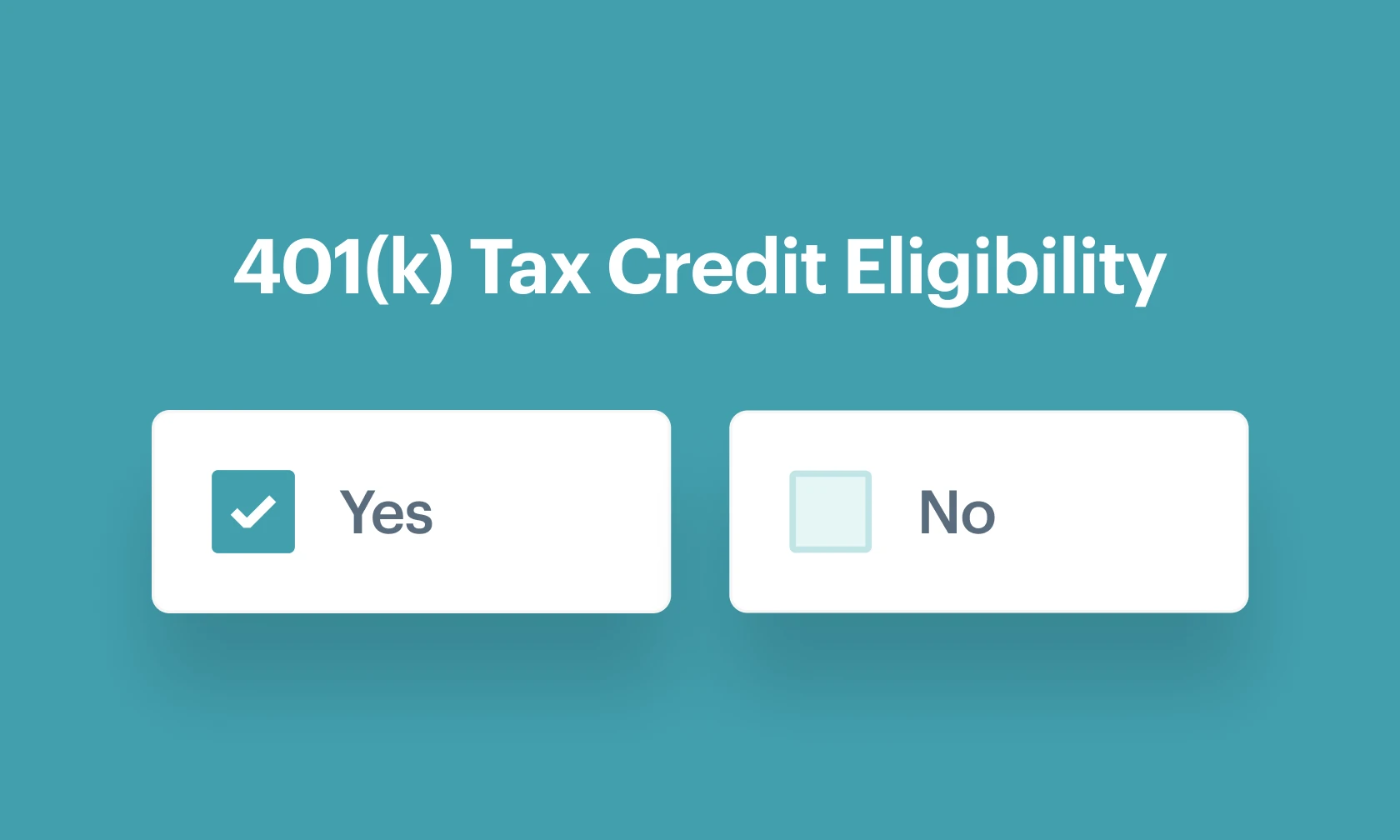

If you’re a small business owner considering a 401k plan for your employees, navigating the intricacies of tax credits and setup costs can be daunting. To simplify this process, let’s break down the 401k Setup Tax Credit and what it really means for your business.

1. Eligibility and Covered Expenses:

Small businesses with 100 or fewer employees who earned at least $5,000 last year and have not had a retirement plan in the past three years qualify for this tax credit. The credit can help cover the initial costs associated with setting up the 401k plan, including administrative fees and employee education about the plan.

2. Amount of the Credit:

You can claim 50% of your setup costs, up to a maximum of $5,000 per year for the first three years. This means the total potential savings could reach up to $15,000.

3. Upfront Costs:

Despite the tax credit, you’ll need to pay all initial costs of setting up and administering the plan. These expenses include fees for plan setup, administrative services, and employee training sessions on plan benefits.

4. Claiming the Credit:

After paying these initial costs, you can claim the tax credit when you file your annual business taxes. This credit reduces your tax liability; however, if the credit amount is more than your tax due, the excess won’t be refunded and can’t be carried to other tax years.

5. Ongoing Costs After Credit:

It’s crucial to understand that after the first three years, you’ll be responsible for all ongoing costs of the plan. These include yearly administrative fees and any other expenses necessary for maintaining the plan.

6. Fiduciary insurance:

Employers need fiduciary insurance for their 401k plans to protect themselves against liability for breaches of fiduciary duties. Managing a 401k involves making critical decisions about plan management and investments, and fiduciary insurance helps cover legal fees, settlements, and other costs arising from claims of mismanagement or negligence.

7. Shutting down a 401k plan:

Shutting down a 401k plan can be a complex and costly process, requiring meticulous administrative work. This includes filing final forms with the IRS, distributing all assets to participants, and possibly incurring penalties for early termination. The decision to close a 401k is significant, both in terms of procedural burden and financial impact on the employer.

Practical Implications for Small Business Owners:

Financial Planning: Ensure you have the necessary upfront cash to cover the initial setup costs. The tax credit is beneficial, but it doesn’t provide immediate cash flow since it only affects your tax liabilities when you file.

Long-term Budgeting: Plan financially for the ongoing costs of maintaining the plan beyond the initial three years.

Business Cash Flow: Assess your business’s cash flow to ensure it can handle the recurring costs of the 401k plan without relying solely on the tax credit.

Additional considerations:

New 401k plans require auto-enrollment of all employees.

Matching contributions have to be paid to all employees in a safe-harbor plan.

401k plan audit costs should also be factored into your budgeting considerations.

As you consider setting up a retirement plan for your small business, it’s essential to explore all your options. While the 401k Setup Tax Credit may provide an incentive, it’s worth noting that these plans can still be financially burdensome in the long run. At Icon, we offer an alternative solution with our Portable Retirement Plan (PRP). Designed to be both high-quality and affordable from the start, the PRP eliminates the need for tax credits while still providing your employees with a robust retirement savings option. By choosing the PRP, you can enjoy the benefits of a top-tier retirement plan without the hefty price tag, helping lead your business and your employees to a more secure financial future.

Are you worried about retirement savings? You’re not alone. According to a recent study by the Employee Benefit Research Institute (EBRI), only 52% of workers are confident they’ll have enough money for retirement. But there’s good news – offering a retirement plan to your employees can help.

At Icon, we understand that offering a retirement plan can be a daunting task for small business owners. That’s why we’ve created a solution that’s easy to set up, affordable, and designed specifically for businesses like yours. Our Icon Portable Retirement Plan (PRP) is the perfect choice for small and medium-sized businesses looking to offer a retirement plan.

Our plan is fully automated and can be set up in just 5 minutes. We take care of the regulatory complexity and fiduciary burden that comes with traditional retirement plans. And best of all, our plan is a turnkey solution for you and your employees at a fraction of the cost of a 401k plan. With the Icon PRP, you can offer your employees a retirement plan that’s easy to manage and cost-effective.

But why offer a retirement plan in the first place? The EBRI study found that workers who have access to a retirement plan are more likely to save for retirement. In fact, 87% of workers who have access to a plan participate in it, compared to just 44% of workers who don’t have access. And workers who participate in a plan are more confident about their retirement savings – 72% of participants are confident, compared to just 42% of non-participants.

Offering a retirement plan can also help you attract and retain top talent. The EBRI study found that retirement savings is the most wanted benefit after healthcare. By offering a plan, you can show your employees that you care about their financial well-being and help them save for their future.

The Icon PRP is designed specifically for small and medium-sized businesses. It’s easy to set up and manage, and it’s a cost-effective solution that helps you attract and retain top talent.

Schedule a call with us today to learn more about how we can help you offer a retirement plan that works for you and your employees. We’re here to help you achieve your business goals and ensure a brighter future for your team.

In recent years, the trend of using BNPL (Buy Now, Pay Later) services has grown exponentially, with millions of people taking advantage of the convenience of these services. However, while BNPL services may seem like an attractive option for many, the truth is that these services can be harmful to your financial health, contributing to increasing consumer debt and financial insecurity.

According to data from the Federal Reserve, consumer debt in the United States has risen to record levels in recent years, surpassing $14 trillion in 2020. While there are many factors contributing to this trend, the rise of BNPL services is undoubtedly a significant factor.

One of the biggest issues with BNPL services is the high-interest rates and fees associated with late payments. While many BNPL services offer low or no-interest rates for short-term loans, the fees and penalties for missed or late payments can quickly add up. In fact, some BNPL services charge fees as high as 30% for missed or late payments, making it difficult for consumers to get out of debt once they have taken on a balance.

Additionally, BNPL services can encourage overspending and impulse buying. With the convenience of these services, consumers may be more likely to make purchases they can’t afford, leading to further financial strain in the long run.

Another issue with BNPL services is that they may not be a good option for people with poor credit. Many BNPL services require a credit check, and those with low credit scores may not be approved or may be subject to higher interest rates and fees.

The impact of BNPL services on your credit score is worth considering. Late or missed payments can harm your credit score, making it more difficult to secure loans or credit in the future.

While BNPL services may be a convenient option for some, it’s important to consider the long-term consequences before you take on additional debt. Be aware of the fees and penalties associated with these services and consider whether you can realistically afford to take on additional debt. In many cases, it may be better to save up for the things you want rather than relying on BNPL services to make purchases.

With increased consumer debt and potential financial insecurity, it’s important to consider alternative options for financing purchases and to use BNPL services with caution. In most cases, it’s better to save up for the things you want rather than taking on additional debt with BNPL services.

It’s true, the Boomer generation (Americans born between 1946 and 1964) is the wealthiest generation in U.S. history. They have a greater percentage of wealth heading into retirement than the two generations before them, and they were wealthier in their younger years than millennials are now. In fact, they held 21% of U.S. wealth when they were the age millennials are now, while millennials hold just 6% of U.S. wealth. They’ve been better savers and yet, many baby boomers are still facing financial crises in retirement.

What’s Happening

A confluence of factors that include early forced retirement, inflation, medical crises, increased debt, recent market fluctuations and a fewer percentage of workers with pensions has created a wealth gap between what baby boomers will need in retirement and what they have.

According to 2019 data from the Employment Benefit Research Institute (EBRI), the median nest egg for a family headed by a 60-65 year old whose annual income was between $71,000 and $126,000, was about $150,000. For people making above $126,000, the average jumped to $535,000. Medicaid and social security are available to supplement retirement savings, and 40% of retired individuals depend on these programs to pay for day-to-day expenses. But even with their support, the EBRI estimates 40% of Americans aged 35-64 are still at risk of experiencing a shortfall in retirement savings during their lifetimes.

That’s because people have underestimated how much it will cost to retire. Expenses include the everyday costs of mortgage, rent, food and utilities, but these pail in comparison to the $315,000 the average couple who retires today can expect to pay in medical expenses in retirement. Additionally, there’s the cost of long-term care which can reach $180,000 a year.

People just aren’t saving enough to keep up with the rising cost of living and the fact that we’re all living longer. But it’s not their fault.

How We Got Here

The baby boomer generation is a kind of transition generation. Before them, the Greatest generation and the Silent generation mostly enjoyed pensions that guaranteed a steady stream of income in retirement. Their life expectancy was also a lot lower so there were fewer non-working years they had to save for. Now, only 15% of workers have pensions so the burden of saving for retirement falls squarely on their shoulders and they’re living longer– sometimes 40 years past retirement. But the retirement savings vehicles haven’t caught up to this new reality.

For the most part, large companies replaced the pension with a 401k in the 1970’s and because of this, workers, who were for the most part, not financial experts, became responsible for investing their retirement savings. Their options were limited to the investments their employers chose to include in their 401k plans and these accounts often charged (and still charge) high fees that ate into baby boomers’ savings. In addition, these portfolios weren’t always managed in the best interests of the plan participants. The investments offered were often those that made fund managers money as opposed to those that contributed to a well-diversified, low-cost portfolio. In fact, a recent study found that baby boomers’ 401ks were heavily invested in stocks, making them vulnerable to recession.

In addition to longer life expectancy and a less secure source of retirement income, many baby boomers have experienced early forced retirement. Whether the cause was a medical issue (theirs or their partner’s) or economic fluctuations that left them unemployed late in their career, many baby boomers have been prematurely cut off from contributing to their 401k, making it more difficult to grow their nest egg.

Recent spikes in inflation and the fact that more than half the families headed by a 75 year old carry debt (versus in 1992 when just ⅓ of families headed by a 75 year old carried debt) mean that their savings won’t go as far as they’d originally planned.

But there is a way to fix this for Boomers and the following generations.

How Icon can Help

One of the worst things that can happen to a worker of any age is being cut off from the ability to save for retirement. This happens because 401ks aren’t portable. They’re tied to the employers through which they’re offered and once a worker is no longer employed with the company, they can’t contribute to that account. They must roll it over to a new employer’s 401k (which can be costly and complicated) or they can leave the money where it is and start a new account with a new employer (which is inefficient), or, worst-case-scenario, they’re working for themselves or for another company that doesn’t offer a 401k so they’re left without any retirement savings vehicle altogether.

That’s where Icon can help. An Icon Retirement Savings account is portable and accepts 401k rollovers so workers who have found themselves prematurely locked out of saving for retirement can ensure they meet their savings goals without managing more than one account. This also applies to workers who change companies frequently and those who work for themselves. Icon is a retirement savings plan that covers every type of worker so that everyone can save for their future.

In addition, Icon isn’t structured to make money off of the investments in our portfolios. We don’t receive kickbacks like many investment management firms so our portfolios are designed to be low-cost and offer a diverse selection of assets.

You can also contribute to a 401k and an Icon plan in the same year so for those nearing retirement that want to max-out their retirement savings opportunities, Icon is an additional investment tool. However, if you’re covered by a 401k at your employer and you’d like to contribute additional money to an IRA (like Icon), your ability to deduct your contributions from your gross taxable income will be limited based on your annual income and how you file your taxes.

Icon Retirement Savings plans are designed to help workers of every stage of life reach their retirement goals. They’re flexible, portable, cost effective and structured so that plan participants get to keep, and keep investing, more of their money. It’s one of the most promising solutions to the retirement crisis we’re seeing today.

San Francisco, California—Icon today announced a partnership with Proliant, a leading provider of cutting-edge Human Capital Management (HCM). This collaboration brings Icon’s simplified and cost-effective PRPs (Portable Retirement Plans) to Proliant’s clients.

The partnership combines Icon’s streamlined retirement solution with Proliant’s HCM expertise, delivering a radically simplified user-experience. Our PRPs offer features like rapid 5-minute plan setup, hands-off administration, regulatory simplicity, and seamless plan portability.

“At Icon, we prioritize simplicity, transparency, and security as the cornerstones of our customer philosophy”, said Alexander Mace, Icon’s Chief Technology Officer. “Our PRPs are designed to help both businesses and individuals with a simplified user experience with smart default choices built-in, all while being extremely affordable and less complex than the 401k system.”

The integration empowers Proliant customers to set up their Icon plan in minutes ensuring quick implementation. The turnkey Icon platform handles all plan administration, and the integration with Proliant means that employers can manage their retirement plan with little to no involvement.

This partnership is a significant step toward our shared vision of a financially secure future for all. Together, Icon and Proliant are reshaping retirement benefits, providing practical solutions for today and tomorrow.