Reach your long-term wealth goals with smart features and simplified investing.

Icon makes saving and investing easy and optimized for your needs.

Offered to Kinly users

No minimums to enroll.

Savings are tax-advantaged

You can save up to $6,000 or $7,000 a year if you’re over 50.

Invest in smart portfolios

Savings will be invested in a low-cost portfolio tailored to your needs with investments from leading asset managers like Vanguard and BlackRock.

Easy to use

Smart choices are built in, we take the guesswork out of investing.

It only takes 5 minutes to set up.

Here’s how it works:

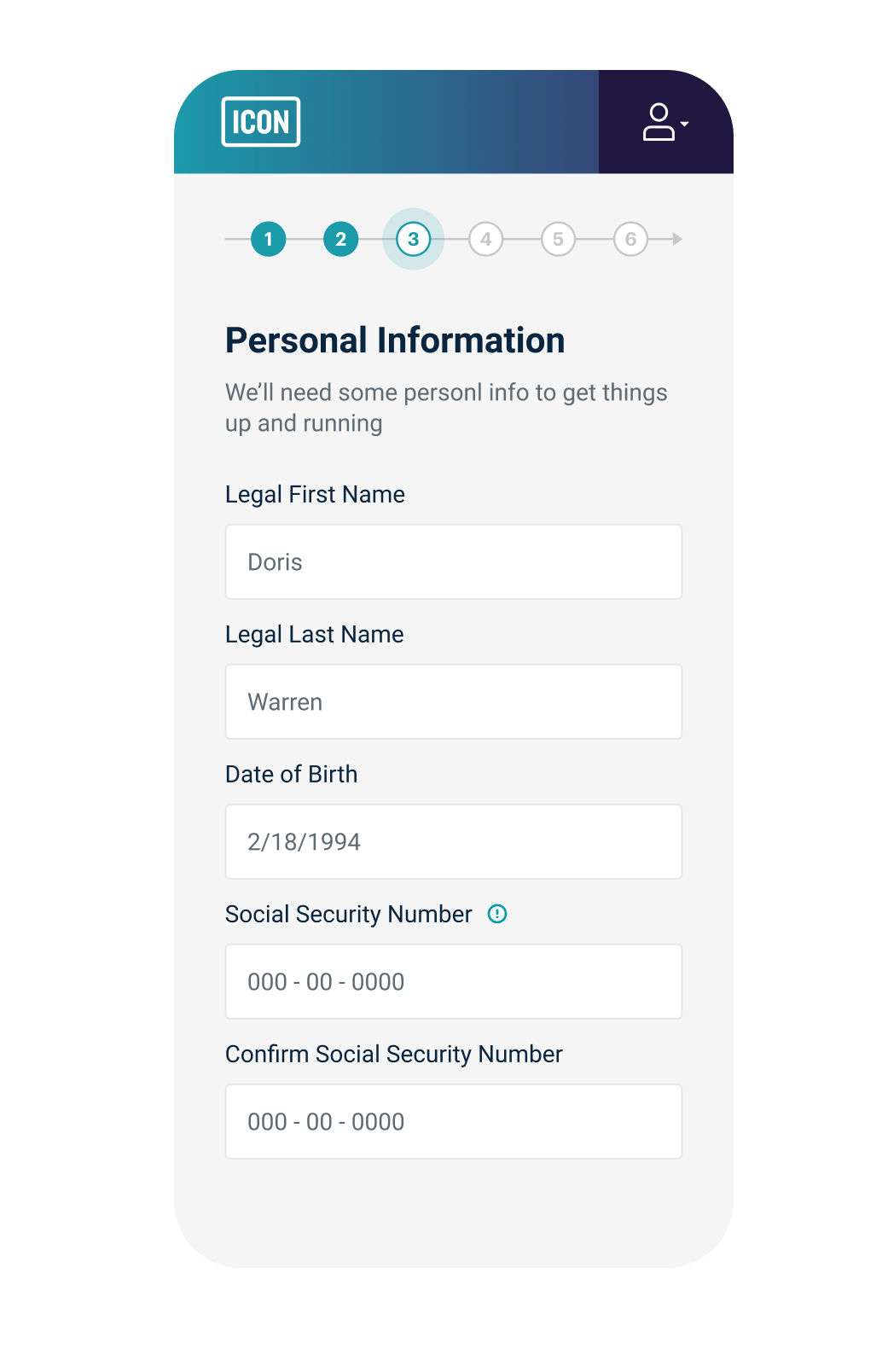

Create your account.

It's easy to set up.

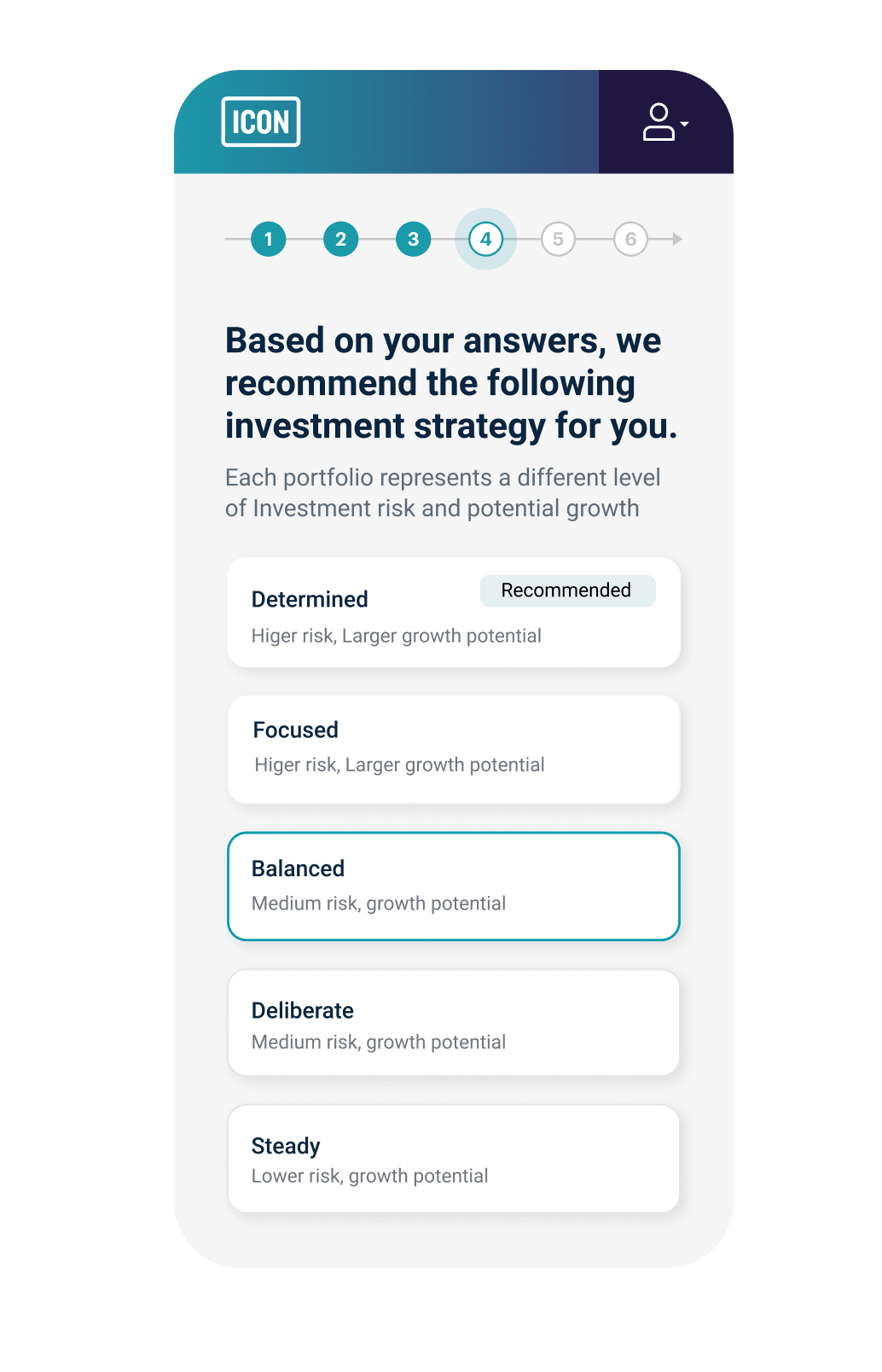

We’ll recommend a portfolio.

You don’t have to be a financial expert, you don’t have to choose funds, or rebalance. Icon does all of this for you.

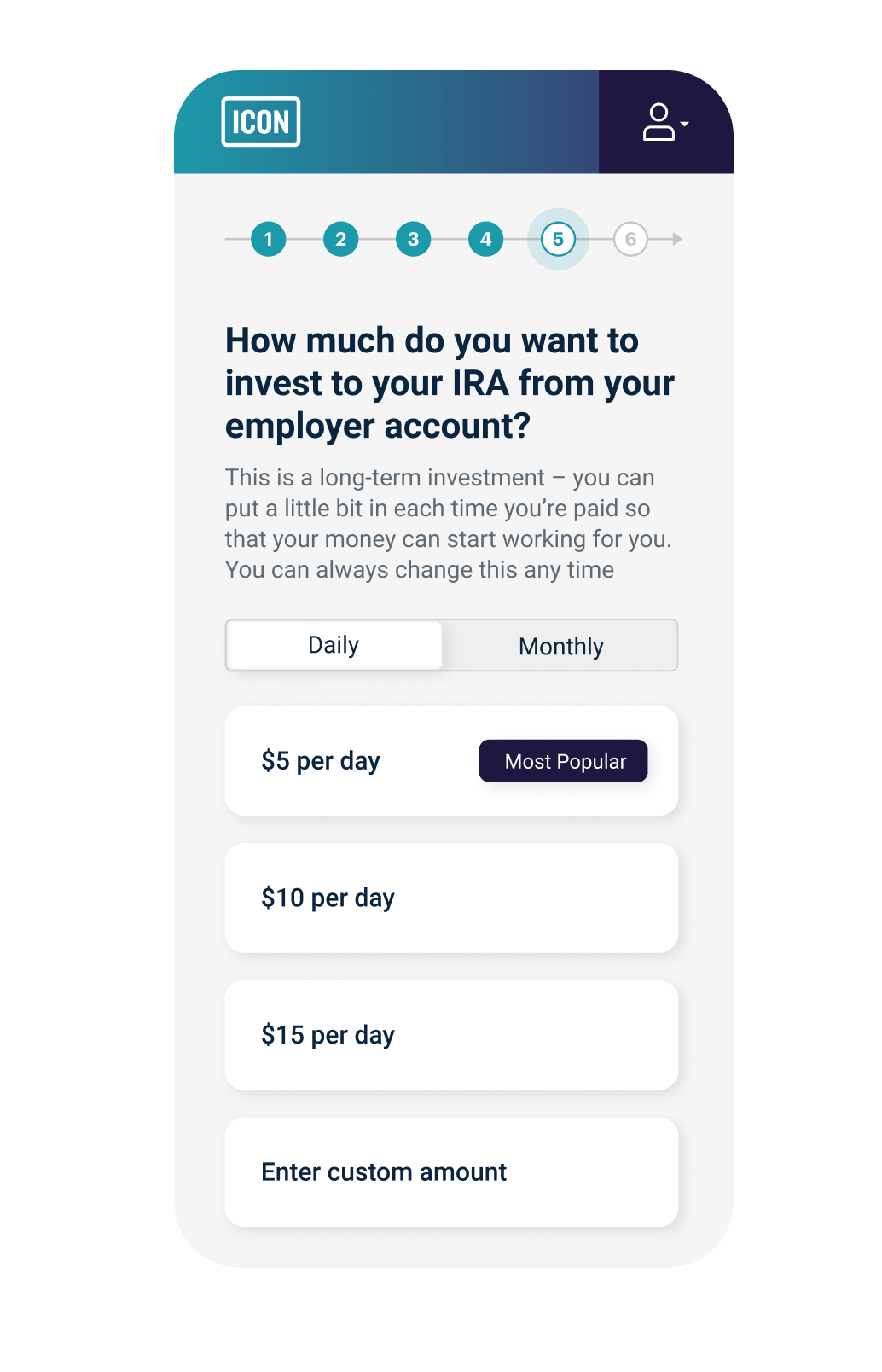

Start saving.

You decide how much to contribute— up to $6,000 annually or $7,000 if you're over 50.

Save smarter with an Icon Personal Retirement Plan.

Low fees

Low fees mean you keep more of your money.

Smart portfolios

It's your personal plan, with investments tailored to your needs.

Portable

Fully portable, it follows you from job to job. No rollovers.

Investing is the key to wealth building. Icon makes it easy.

Just answer a few questions, and we’ll give you a portfolio tailored to your needs with diversified, low cost index funds. Your Icon smart portfolio handles all of the rebalancing and keeps an eye on your plan and give you helpful tips along the way to make sure you are on track.

Low fees mean you keep more of your money.

Retirement plans often charge high fees that erode your savings. We don’t make money on your investments or trade activity. Instead we charge a flat monthly fee of just $4.00.

Your money is in good hands.

Icon portfolios are built with low-cost, high quality investments from the most respected asset managers in the world: Vanguard and BlackRock.

Your investments grow tax-free.

Your Icon retirement account is a traditional IRA and as long as your money remains in the account, you pay no taxes on the investment growth. Your annual contributions may be tax-deductible.

Turns out, you can take it with you.

Your Icon plan is portable, which means as your life changes your plan follows you from job-to-job. It doesn’t require a rollover and you can continue to use your plan, at your next job or through your own bank account.

We're here if you need us.

You can do everything you need in your dashboard. If you have questions about your plan, you can find answers in our Retirement & Financial Wellness 101. But sometimes, it’s easier to chat with someone. Feel free to contact us.

Still have questions?

Question about contribution amounts?

For 2022 the total contributions amount you can make for this calendar year are $6,000 or $7,000 if you are over 50.

Can I have Multiple IRA’s?

It is not unusual for people to have more than one IRA. The most you can contribute to an IRA annually is $6,000 or $7,000 if you are over 50.

Example

Korri is maxing out her annual contribution every year in her Icon Personal Retirement Plan offered through her employer. She is also holding an IRA account that has rollovers from a previous job. She can maintain her old IRA, and still max out her Icon plan.

What kind of tax-advantaged account is the Icon Personal Retirement Plan?

Your Icon retirement plan uses an Individual Retirement Account. We this type of plan because we don’t like the limitations, the complexities, and the high fees that come with 401k accounts. With an IRA we can easily optimize for your needs. You always have control over your plan, your investments are based on your preferences, and you never have to do a rollover or worry about a lost account.

Can I rollover old 401k plans into Icon?

Yes, for more information contact us.

Can I borrow from my Icon account?

You generally cannot take a loan from an IRA. You can make withdrawals to meet specific needs.

- A qualified first-home buyer distribution

- For higher education expenses

- If you become permanently disabled

- For the birth or adoption of a child